Right here at TPG, we love credit cards. We’ve skilled the facility of redeeming bank card rewards, and we wish to assist everybody else have that nice expertise.

However in case you’re new to the world of bank cards, studying a bank card utility (or perhaps a review) could make you’re feeling such as you missed a course someplace everybody else seems to have taken. If that’s you, you’re in the appropriate place.

Beneath, we’re taking the thriller out of bank cards. We cowl all the pieces from phrases to forms of bank cards and even breaking down a bank card invoice. So settle in, perhaps seize a notepad, and let’s get into it.

Bank card debt

Earlier than we go over the rest, it’s essential to notice that whereas we’re large followers of bank cards at TPG, we by no means suggest carrying a steadiness from month to month. Carrying a steadiness means you’ll be charged curiosity, which prices you excess of the worth you’ll get from any rewards you earn.

For those who’re contemplating a bank card, first be sure you have a plan to remain inside your price range and repay your steadiness every month. By no means cost a purchase order to a bank card except you’re 110% certain you possibly can pay it off when your invoice is due.

Associated: Credit card debt hits new record of over $1 trillion — here’s how to consolidate and pay off your debt

Credit score scores

A credit score is a quantity — normally between 300 and 850 — that potential lenders use to find out their danger in lending you cash.

Your credit score rating is made up of a number of components, together with fee historical past, the quantity you owe and new credit score opened. To construct and hold a very good credit score rating, you could borrow and pay it again on time. Utilizing your bank card and paying your steadiness in full every month is an effective way to improve your credit score.

Reward your inbox with the TPG Day by day e-newsletter

Be part of over 700,000 readers for breaking information, in-depth guides and unique offers from TPG’s consultants

Whenever you apply for any sort of credit score, together with a bank card, the potential lender will test your credit score rating to assist them determine whether or not or to not approve your utility. Usually, the perfect rewards playing cards require good to glorious credit score scores for approval.

Nonetheless, in case your rating is lower than stellar, don’t fear. We will present you methods to improve your credit score and methods to earn rewards while you’re improving your credit.

Associated: How to check your credit score for free

Debit vs. bank cards

Whenever you use a debit card, cash is pulled straight out of your checking account to cowl your buy. That’s why your $1,000 buy will likely be declined in case you solely have $500 in your checking account.

Nonetheless, whenever you use a bank card, you borrow cash from the bank card firm to make your buy. Whenever you repay your steadiness, you’re paying them again on your mortgage. For those who fail to pay inside the given timeframe (usually round a month), you’ll be charged charges and curiosity, and your credit score rating may drop.

The primary good thing about utilizing a debit card is that it retains you from overspending. For those who use a bank card responsibly, nevertheless, you’ll earn rewards, get extra advantages and enhance your credit score rating.

Associated: Why a credit card is a smarter choice than a debit card

Learn how to learn your bank card invoice

The phrases, dates and completely different numbers on a bank card invoice could make studying one really feel like a decoding exercise. Nonetheless, the excellent news is that the code may be simply damaged by understanding some key phrases.

First, let’s make clear the phrases “invoice” and “assertion.” Earlier than on-line banking, cardholders obtained a paper assertion (additionally referred to as a invoice) within the mail every month. That assertion would define the cardholder’s prices for the billing interval (the time for the reason that final invoice), assertion steadiness (quantity the cardholder charged throughout the billing interval), minimal fee quantity and fee due date.

Now, we have now the posh of checking our accounts on-line at any time. We nonetheless have statements that replicate our billing intervals, however we are able to additionally see the transactions we’ve made since our final assertion. This additional info is sweet, however it will probably make issues a bit complicated.

Right here’s a breakdown of what you may see whenever you log in to your on-line account:

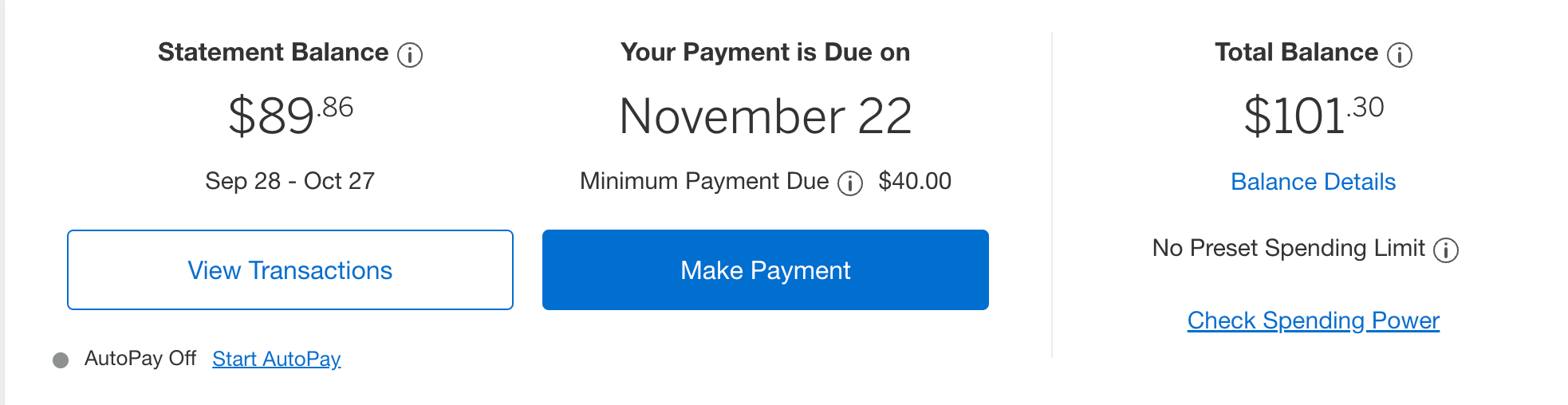

The assertion steadiness is the quantity charged throughout your most up-to-date billing interval. You could pay this quantity by the due date to keep away from being charged curiosity or late fee charges.

The due date on your billing cycle depends upon your card (you’ll find this in your card’s phrases and circumstances).

Within the instance above, the cardholder should pay their assertion steadiness of $89.86 by the Nov. 22 due date to keep away from charges.

The minimal fee is the bottom quantity you possibly can pay by the due date to keep away from being charged a late fee price. Nonetheless, in case you solely pay the minimal fee (or something decrease than the complete assertion steadiness), you’ll carry a steadiness over to the following billing interval and be charged curiosity on that quantity.

The “complete steadiness” refers back to the whole quantity that you simply owe in your card: the assertion steadiness from the earlier month, together with any prices which were made since that billing cycle closed. On this instance, the cardholder has charged $11.44 for the reason that time limit, so the overall steadiness is the assertion steadiness of $89.85 plus the latest prices of $11.44. The cardholder will pay the overall steadiness, however they’ll additionally simply pay the assertion steadiness and nonetheless keep away from paying any charges. In the event that they do that, the $11.44 will present up on the following invoice, which they’ll should pay the following month.

One other quantity you’ll doubtless see is “accessible credit score,” which is the quantity left in your credit score restrict. This quantity will fluctuate as you repay your steadiness or cost extra to your steadiness. For instance, if this person’s credit score restrict have been $4,000, their accessible credit score can be $3,898.70 (the overall steadiness of $101.30 subtracted from the credit score restrict of $4,000). Keep away from maxing out your credit score restrict, as your card could also be declined or charged an over-the-limit price.

Associated: After 15 years, why the Chase Sapphire Preferred should still be your first rewards card

Charges and charges

Now that you simply perceive methods to pay your bank card invoice, let’s assessment all of the important charges a bank card firm may cost.

- Annual proportion price (APR): The rate of interest charged for the complete yr. There are numerous forms of APRs, together with steadiness switch, money advance, penalty and buy APRs. The most typical sort of APR is your buy APR. That is the month-to-month rate of interest that is added to your bank card steadiness if you don’t pay your assertion steadiness on time.

- Introductory APR supply: A reduced APR for a defined period may also help you keep away from extra curiosity prices on purchases and steadiness transfers.

- Annual price: The cost of owning your card, charged as soon as per yr. Some playing cards haven’t any annual charges, whereas others can cost as much as $895 (or extra) per yr.

- International transaction price: The quantity charged to your account when paying with a overseas forex. Some credit cards waive foreign transaction fees, whereas others cost charges. That is usually 3% of every transaction.

- Late fee price: The quantity charged to your account whenever you fail to pay the minimum payment by your fee date. Along with the penalty APR charged to your steadiness, you’ll even be charged a late fee price.

- Over-the-credit-limit price: The quantity charged to your account whenever you exceed the credit score restrict outlined in your card.

- Return fee price: The quantity charged to your account when the fee technique you supplied on your bank card assertion fails or bounces for causes akin to inadequate funds, account freezes or closures.

Associated: How to choose a credit card with 0% APR

Kinds of bank cards

For those who’re new to bank cards, the sheer quantity of choices can really feel overwhelming. It helps to slim your search by first figuring out which sort of bank card you need.

Listed here are the most typical bank card varieties.

Common journey

These bank cards earn journey rewards and include journey perks that aren’t tied to any airline or resort model. They usually earn transferable rewards, that are our favourite sort as a consequence of their excessive worth and suppleness.

These playing cards additionally normally include normal journey advantages, akin to travel insurance, TSA PreCheck/Global Entry credit and airport lounge access.

For our prime picks, try our full list of the best travel credit cards.

Associated: Why transferable points are worth more than other rewards

Airline

Airline bank cards are playing cards tied to 1 particular airline.

You’ll earn rewards within the type of that airline’s factors or miles and get perks tied to the airline, akin to free checked luggage, computerized elite standing and airport lounge entry.

Associated: Best airline credit cards

Lodge

Lodge bank cards are tied to a particular resort model.

You’ll earn rewards within the type of factors that you need to use for any resort inside that model, and also you’ll get perks like free nights and computerized elite standing.

Associated: Best hotel credit cards

Money-back

Cash-back cards normally have the best rewards to earn and redeem. With a cash-back card, you’ll earn a proportion of your buy again in rewards.

Then, you possibly can redeem your rewards for money — both as a press release credit score, a test within the mail or a direct deposit into an eligible checking or financial savings account, relying on the issuer.

Associated: How to choose a cash-back credit card

Secured

A secured credit card is an efficient choice when you’ve got restricted credit score historical past or a low credit score rating. With a secured card, you’ll pay a safety deposit whenever you open the cardboard, which features as insurance coverage for the bank card firm.

Typically, these don’t earn rewards, however they’re a great way to construct your credit score and improve your possibilities of being accredited for a rewards bank card afterward.

Associated: Best secured credit cards

Pupil

A pupil bank card is for — you guessed it— school college students. They’re designed to assist college students construct credit score, good monetary habits and a relationship with a financial institution so that they’ll be prepared for a extra superior bank card once they graduate.

These are inclined to earn minimal rewards, however they’re a wonderful choice for college students to ease into the world of bank cards.

Associated: The best credit cards for college students

Approved person

A licensed person is somebody who has been added to an present bank card account by the first account holder. A licensed person has full spending talents on their bank card, however normally has limited benefits.

For those who’re having bother getting accredited for a bank card, being added to another person’s account as a licensed person could assist your credit score rating.

Associated: Have good credit? Share it with an authorized user

Incomes rewards

Every rewards card earns a kind of rewards “forex.” The American Express® Gold Card earns transferable American Express Membership Rewards points, for instance, whereas the Citi® / AAdvantage® Executive World Elite Mastercard® (see rates and fees) earns American Airlines AAdvantage miles, and the Hilton Honors American Express Surpass® Card earns Hilton Honors points. These currencies have completely different values, so try our newest TPG valuations chart to see what every rewards sort is price.

Your card’s incomes price and spending habits decide the quantity of rewards you’ll earn. Some playing cards earn at a fixed rate, which means they earn the identical quantity on all purchases. The Capital One Venture Rewards Credit Card, which earns 2 Capital One miles per greenback spent, and the Citi Double Cash® Card (see rates and fees), which earns 2% money again on all purchases (1% whenever you purchase and 1% as you pay), are each examples of playing cards that earn at a set price.

Different playing cards have bonus-earning classes. The Chase Sapphire Preferred® Card (see rates and fees) , for instance, earns 3 Ultimate Rewards points per greenback spent on dining (together with takeout and eligible supply companies), widespread streaming companies and on-line grocery purchases (excluding Walmart®, Goal® and wholesale golf equipment) in addition to 2 factors per greenback spent on travel purchases. It earns 1 level per greenback spent on all different purchases.

Moreover, many rewards playing cards embody welcome bonus that may be price a whole lot or hundreds of {dollars} in worth. To earn the welcome bonus, you’ll must spend a certain amount of money in a given time frame.

Associated: The best credit cards for each bonus category

Bank card finest practices

You could have heard that bank cards must be prevented as a result of they’ll get you into critical bother. Though you received’t hear us let you know to keep away from bank cards, we solely condone accountable bank card use.

Listed here are a number of the finest bank card practices that we dwell by.

At all times pay your steadiness on time and in full. It might seem to be we’re closely emphasizing this level, however it’s for good purpose. Not solely will you negate any factors and miles you earn in case you begin to accrue curiosity prices, however carrying a steadiness can get you into vital debt shortly.

Bank cards should not free cash, so by no means cost greater than you possibly can afford. Equally, do not forget that you’ll owe the assertion steadiness in your card every month. Finances and handle your credit score properly so your funds don’t get out of hand.

Perceive bank card utility restrictions. It’s possible you’ll be tempted to dive into the deep finish of bank card rewards instantly, however it’s finest to take it slowly. Along with giving your self time to discover a bank card price range system that works finest for you, know that some issuers have their very own set of restrictions. It pays to be considerate and have a longer-term plan earlier than you apply for a bank card.

Wait a minimum of three months (ideally, six months or longer) between card purposes. Opening new strains of credit score impacts your credit score rating, and making use of for brand spanking new playing cards too shortly is usually a purple flag. Tempo your self by incomes a card’s welcome bonus and taking a while to find out how nicely the cardboard matches your way of life. Then you possibly can select your subsequent card based mostly on what finest enhances it (and any others in your pockets).

Suppose twice earlier than canceling a bank card. As you add extra playing cards to your portfolio, you is likely to be tempted to cancel those you aren’t reaching for as typically. Nonetheless, if a card has no annual price, there’s no hurt in retaining the cardboard in your pockets — doubtlessly eternally. Size of credit score is a think about your credit score rating, so retaining your earliest playing cards open helps improve your credit score historical past and, subsequently, your credit score rating.

Associated: TPG’s 10 commandments of credit card rewards

Constructing a points-and-miles technique

Now that you’ve got a baseline understanding of bank cards, it’s time to decide on your card.

Don’t really feel like you must have a technique in place proper now. For those who’re overwhelmed by the forms of rewards, you can begin small with a cash-back card to solidify your good credit score habits and revel in easy rewards redemptions.

However in case you do have a dream journey in thoughts, you possibly can set your sights on a journey rewards card that may assist make that dream a actuality.

Whenever you’re prepared to consider a points-and-miles technique, try our TPG guide to getting started with points and miles to travel.

Associated: Key travel tips you need to know — whether you’re a first-time or frequent traveler

Backside line

Congratulations! You’re armed with the phrases and information you must analysis, apply for and responsibly use a bank card.

Now, check out our suggestions of the best first credit cards and use the information you’ve gained right here that can assist you select the one that matches your spending habits and rewards targets. We’ll be right here for you as you undergo each step of your bank card journey.

Associated: The best starter travel credit cards